Making a living with a 44% win rate: expectancy over accuracy

You do not need to be right most of the time. You need to be paid more when you are right than you lose when you are wrong. Here is the math, and how to journal it.

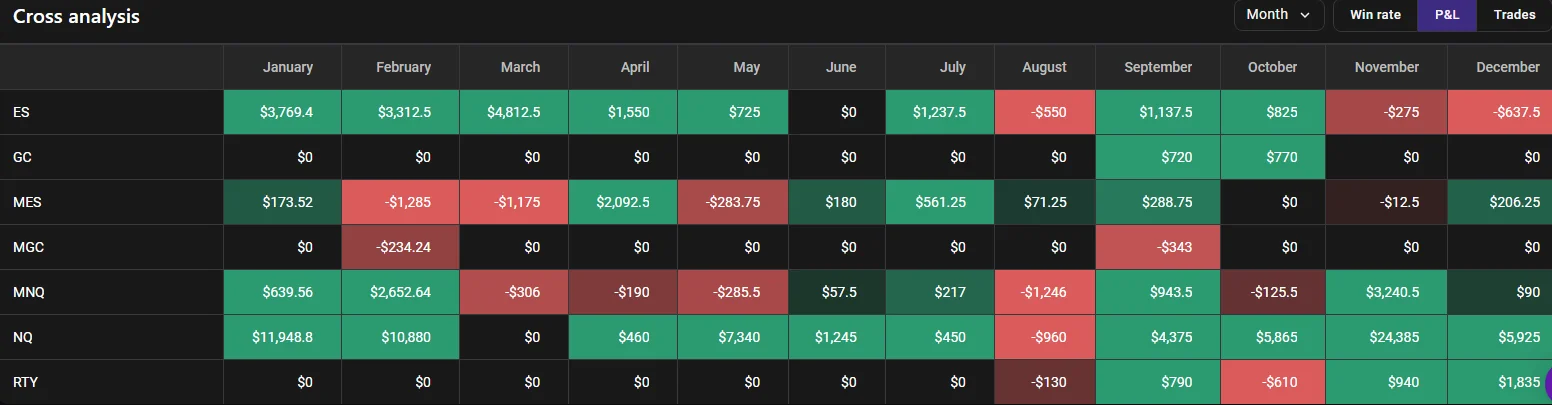

There is a screenshot that circulates every few months: a trader's cross-analysis table, month after month of green, with a headline that reads "I make a living with a 44% win rate." New traders see it and assume it is a trick. It is not. It is just expectancy, and once you understand it you stop caring about being right.

Accuracy is not the product

The market does not pay you for being correct. It pays you the difference between what you make on winners and what you give back on losers, multiplied by how often each happens. A 44% win rate simply means that 44 out of 100 trades close green. That number is meaningless until you attach it to the size of those wins and losses.

Run the arithmetic. Risk one unit per trade. Win 44 trades at an average of 2 units each: +88. Lose 56 trades at an average of 1 unit each: -56. Net: +32 units across 100 trades, a positive expectancy of 0.32R per trade. You were wrong more often than you were right and you still compounded.

The number to journal is R, not dollars

Dollars lie to you because position size changes between trades. A $500 win on a huge position and a $500 loss on a tiny one look identical in a P&L column and mean completely different things. Journal every trade in R — multiples of the amount you risked — and the distortion disappears.

With R logged on every trade you can compute the only three numbers that matter:

- Average win (in R) and average loss (in R).

- Win rate, as context, not as a headline.

- Expectancy = (win rate x avg win) - (loss rate x avg loss).

If expectancy is positive and your risk per trade is sane, you have a business. If it is negative, no win rate will save you.

Why a high win rate is often a warning

Traders chasing accuracy tend to close winners early to lock in the green and hold losers hoping they come back. That behavior manufactures a beautiful win rate and quietly destroys expectancy — the average win shrinks and the average loss balloons. A 44% win rate with clean, let-them-run winners is worth far more than a 65% win rate built on cut winners and hope.

Prove it over a sample

One month is noise. Expectancy only means something across a sample large enough to survive variance — a few hundred trades before you trust the number. Journal in R, tag by strategy, and let the table fill in. When it does, you will stop flinching at losses, because a loss inside a positive-expectancy system is not a mistake. It is a cost of doing business you have already priced in.